When you talk about RBI rate cuts, a common question pops up in every investor’s mind:

👉 “Should I invest now or wait?”

👉 “What do I do with my cash until rates fall?”

You’re not alone.

In times like these, many investors end up keeping cash in hand — waiting for the “perfect moment.” But the truth is, waiting without a plan can cost you more than a wrong decision.

Let’s break this down in simple terms and let me make you understand what to do with your cash during the rate-cut waiting game.

Why People Hold Cash During Rate Cut Expectations

Before jumping into solutions, let’s understand the mindset what people have.

When rate cuts are expected:

- Investors think markets may correct

- Fixed deposit rates may fall

- Bond prices may rise after the RBI rate cut

- Equity valuations may look expensive

So people pause. They wait. They do nothing.

Holding cash feels safe — but safety has a cost.

The Hidden Cost of Holding Too Much Cash

Cash feels comfortable, but over time it quietly loses value.

📉 1. Inflation Eats Cash Silently

- If inflation is around 5–6% and your cash earns nothing, your purchasing power is shrinking every year.

- ₹1,00,000 today ≠ ₹1,00,000 after 2–3 years.

⏳ 2. Missed Compounding Opportunities

- Markets don’t move in straight lines. Often, the biggest gains happen when people are still waiting.

- Trying to time rate cuts perfectly is extremely difficult — even professionals struggle with it.

🧠 3. Paralysis by Analysis

Constantly waiting for:

- One more RBI meeting

- One more inflation print

- One more correction

…leads to no action at all.

And in investing, no action is also a decision you make.

So, What Should You Do with Your Cash?

The answer is not “invest everything” or “stay fully in cash.”

The smart approach is balance + strategy.

Let’s break it down step by step.

1. Park Cash in Liquid & Short-Term Instruments

Instead of keeping money idle in savings accounts, park it where it’s:

✔ Safe

✔ Liquid

✔ Slightly productive

Best Options:

- Liquid mutual funds

- Overnight funds

- Ultra-short duration debt funds

- Short-term bank FDs

These won’t give massive returns, but they:

- Beat savings account returns

- Keep money accessible

- Reduce opportunity cost

This is your “ready-to-deploy” cash.

2. Use Systematic Investing Instead of Lump Sum

If you’re waiting for rate cuts to invest in equities, don’t wait with 100% cash.

Smarter approach:

- Start SIP or STP (Systematic Transfer Plan)

- Invest gradually over 6–12 months

This way:

- You don’t miss market upside

- You don’t risk bad timing

- Emotions stay under control

Remember:

📌 Markets reward participation, not prediction.

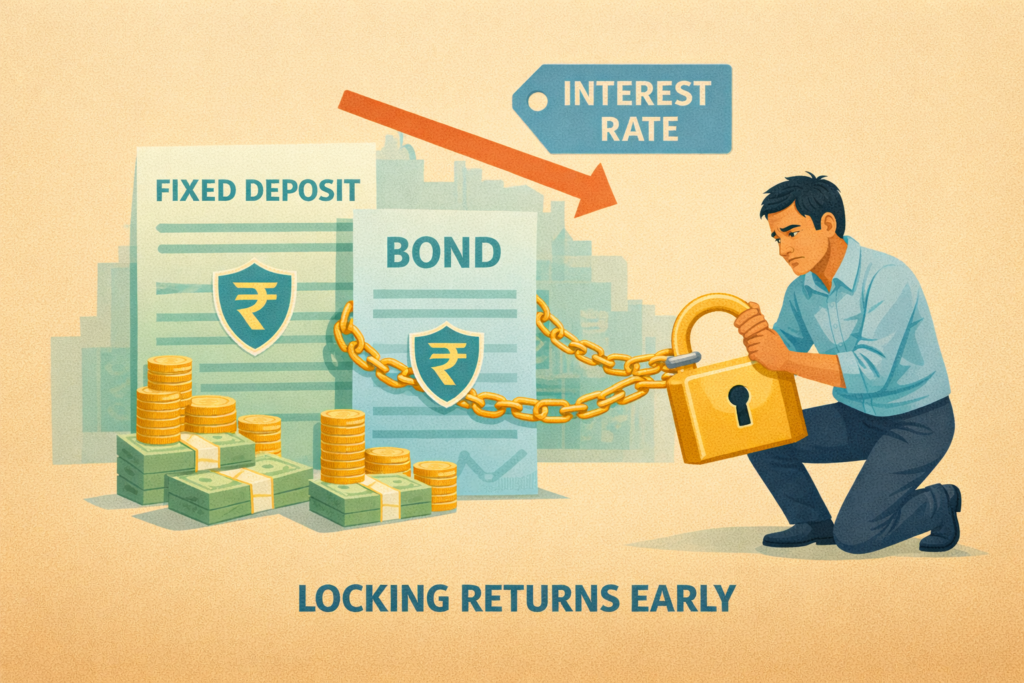

3. Lock Some Fixed Income Before Rates Fall Further

When rate cuts happen:

- FD rates usually go down

- New investors earn lower yields

If you already have cash:

- Lock part of it in medium-term FDs

- Consider debt funds with slightly longer duration

This helps you:

✔ Secure current yields

✔ Reduce reinvestment risk later

Don’t wait for rates to fall to realize you missed better returns.

4. Prepare a “Post-Rate-Cut Shopping List”

Instead of waiting blindly, prepare in advance.

Ask yourself:

- Which stocks do I want to buy?

- At what valuations?

- Which sectors benefit from rate cuts?

Rate-cut-friendly sectors often include:

- Banking & NBFCs

- Real estate

- Auto & consumer discretionary

- Infrastructure & capital goods

When corrections happen, you act — not panic.

5. Keep Emergency Money Separate

This is critical.

Your investment cash and emergency fund should never mix.

Emergency fund:

- 6–12 months of expenses

- Kept in savings / liquid funds

- No market risk

Once this is secure, investing becomes mentally easier — especially during uncertain times.

6. Don’t Chase “Perfect Timing”

This is the biggest mistake in the rate-cut waiting game.

Markets usually:

- Move before rate cuts

- Price expectations early

- Surprise latecomers

By the time the rate cut is announced:

- Markets may already be up

- Bond prices may already reflect the cut

Perfect timing is a myth.

Good strategy is real.

7. Think in Asset Allocation, Not Predictions

Instead of asking:

❌ “When will RBI cut rates?”

Ask:

✅ “How much should I allocate to equity, debt, and cash?”

Example:

- Equity: 60%

- Debt: 30%

- Cash: 10%

Rebalance when needed.

Let discipline do the heavy lifting.

Common Mistakes to Avoid During Rate Cut Phases

🚫 Sitting entirely in cash for years

🚫 Jumping in all at once after headlines

🚫 Chasing risky assets out of boredom

🚫 Constantly changing strategy with news

Markets punish impatience more than mistakes.

Final Thoughts: Cash Is a Tool, Not a Strategy

Holding cash is not wrong.

Holding cash without a plan is.

The rate-cut waiting game rewards:

✔ Preparation

✔ Discipline

✔ Gradual action

Not fear. Not perfection. Not prediction.

Use this phase to:

- Park cash smartly

- Invest systematically

- Prepare for opportunities

- Stay emotionally calm

Because in investing, time in the market beats waiting for the right time.

Read More: Important Finance Terms You Must Know

Pingback: Godrej Consumer Products Financial Model: How I Built a DCF Valuation in Excel - The EquityVerse

It was really well written mate. I really liked it to be honest. Keep up the good work.