A ₹440 crore Gujarat-based packaging exporter with 46.7% RoCE and clients like Cargill and KRBL is opening its books. Here’s the complete breakdown — financials, valuation, brokerage views, and the risks worth understanding before you apply.

What is Knack Packaging?

Knack Packaging Limited is an Ahmedabad, Gujarat-based manufacturer of Printed and Laminated Woven Polypropylene (PLWPP) bags — the heavy-duty, branded bulk bags used to pack everything from rice and pet food to chemicals and fertilisers in quantities of 5kg to 50kg. Founded in 2013, the company has built an integrated, vertically-controlled manufacturing operation that converts raw polypropylene granules into finished, custom-printed packaging — all under one roof.

This isn’t a small domestic player. Knack Packaging serves over 1,950 customers across 71 countries, with a client roster that includes globally recognised names like Cargill, KRBL, Drools, and Ebro Foods. The company operates a B2B2C model — it sells bags to brands, who then use them to package and sell products to end consumers, meaning the bags themselves carry branding, anti-counterfeiting features, and shelf appeal for the end customer.

Manufacturing happens at a large-scale facility in Gujarat spanning 1.12 million sq. ft with an annual capacity of 36,400 metric tonnes. The company has also expanded internationally through a wholly-owned South African subsidiary and a 50% joint venture in Mexico, which went live in April 2026 to deepen its presence in the Latin America-US export corridor.

IPO Snapshot — Key Details

Note: GMP for this IPO has fluctuated meaningfully in the run-up to listing — reports through late June showed figures ranging from ₹11 to ₹23. Treat any single-day GMP reading as a sentiment snapshot, not a forecast.

The Financials: Strong, Consistent, and Improving

This is where Knack Packaging‘s case gets compelling. Revenue grew from ₹518 crore in FY23 to ₹823 crore in FY26 — alongside that, PAT margins expanded from 3.83% to 11.26% over the same period, a near-tripling of profitability as a share of revenue. That kind of margin expansion alongside revenue growth is a meaningfully positive signal; it means the company isn’t just growing bigger, it’s growing more efficient.

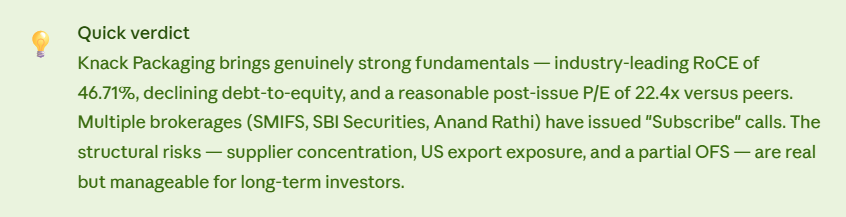

The two numbers that matter most here are RoCE of 46.71% and declining debt-to-equity from 1.29 to 0.62. A high RoCE alongside falling leverage is a genuinely rare combination — it tells you the company is generating strong returns on capital while simultaneously becoming less reliant on borrowed money to do it. Compare that RoCE to listed peers: Mold-Tek Packaging sits at 15.27% and TCPL Packaging at 24.40%. Knack’s profitability tier is meaningfully higher than both.

| Metric | FY23 | FY24 | FY25 | FY26 |

|---|---|---|---|---|

| Revenue (₹ Cr) | 518 | — | 747.38 | 843.77 |

| PAT (₹ Cr) | — | — | 73.81 | 92.72 |

| PAT Margin | 3.83% | — | ~9.9% | 11.26% |

| Gross Profit Margin | — | — | — | 41.85% |

| EBITDA Margin | — | — | — | 20.42% |

| RoCE | — | — | — | 46.71% |

| RoNW | — | — | — | 35.47% |

| Debt-to-Equity | 1.29 | — | — | 0.62 |

Where the IPO money is going

Of the ₹380 crore fresh issue, the company has earmarked ₹320 crore — the overwhelming majority — for a new manufacturing facility at Borisana, Kadi, in Mehsana district, Gujarat. This new plant is intended to produce PLWPP bags and specialised pinch-bottom bags, expanding both capacity and product mix.

This is a growth-capex story, not a debt-cleanup story. Unlike IPOs where proceeds go toward fixing balance sheet issues, here the bulk of the raise is funding expansion — betting that demand for specialised, export-ready packaging will continue growing. The flip side: capacity expansion takes time to translate into revenue, and greenfield projects carry execution risk around timelines and cost overruns.

Strengths and Risks — The Honest Picture

✅ What’s working in Knack’s favour

- Industry-leading RoCE of 46.71% — nearly 2× TCPL Packaging and 3× Mold-Tek Packaging

- Debt-to-equity nearly halved from 1.29 to 0.62, showing improving balance sheet discipline

- Priced at a discount (22.4x P/E) to both listed peers despite superior return ratios

- Established global footprint — 1,950+ customers across 71 countries, with marquee names like Cargill and KRBL

- First-mover advantage in laser-cut PLWPP technology — a genuine technical differentiator

- Multiple independent brokerages (SMIFS, SBI Securities, Anand Rathi) have issued positive coverage

- Vertically integrated manufacturing — raw material to finished product under one roof, supporting cost control

- South Africa subsidiary and Mexico JV (live since April 2026) deepen export market access

⚠️ Risks worth understanding

- Supplier concentration risk — reliant on verbal arrangements with major suppliers, no long-term contracts

- Customer concentration — heavy reliance on top clients for revenue

- US export exposure — nearly a quarter of revenue from the USA, creating exposure to American tariffs and trade policy shifts

- Export concentration in US/Mexico/South Africa makes up 35.19% of total exports

- Polypropylene raw material price volatility directly impacts margins

- Greenfield Mehsana facility expansion is capital-intensive and carries execution/timeline risk

- Partial OFS (₹59.5 Cr) means a portion of proceeds go to promoters, not the company

- Lower EPS relative to some peers despite stronger return ratios — a nuance worth understanding before applying

How to apply

Retail investors can apply via UPI through any broker — Zerodha, Groww, Upstox, and others all support this. Open your broker’s IPO section, search “Knack Packaging IPO,” select your demat account, enter the lot quantity (minimum 1 lot = 88 shares = ₹14,960 at the upper band; retail investors can apply up to 13 lots / 1,144 shares / ₹1,94,480), submit, and approve the UPI mandate. Funds are blocked, not debited, until allotment.

Key Dates to Remember

Bottom Line

Knack Packaging presents one of the stronger fundamental cases among recent mainboard IPOs — a profitable, export-oriented, technically differentiated manufacturer with return ratios that genuinely outpace its listed competition, priced at a discount rather than a premium to those peers. The brokerage consensus leans positive, which is not always the case for small and mid-cap IPOs.

That said, this is still a capital-intensive industrial business with real customer and supplier concentration risk, a meaningful slice of revenue tied to US trade dynamics, and a partial promoter exit built into the offer. The modest and fluctuating GMP suggests the market isn’t pricing this as a guaranteed listing pop — which, if anything, makes it a more genuine long-term proposition than a speculative one. Read the RHP’s actual financial statements directly, reconcile the figures yourself, and decide based on the business — not the grey market mood of the week.

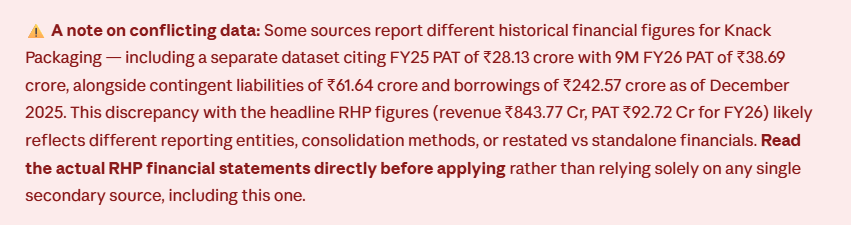

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice or an IPO recommendation. Financial figures are sourced from the company’s RHP and publicly available IPO research and are subject to change; some secondary sources report conflicting figures, so readers should verify directly against the RHP. GMP is unofficial, unregulated by SEBI, and not a guaranteed indicator of listing performance. Brokerage views cited are third-party opinions, not endorsements. Please consult a SEBI-registered financial advisor before applying.

Read More: Advit Jewels IPO Analysis: Should You Apply?