Markets are red. WhatsApp groups are panicking. Your portfolio is down. Before you do anything, read this — a calm, honest breakdown of exactly what’s happening and what your next move should be. It is not a recommendation or an advice to anyone. It is just my personal view to Indian markets. Don’t take any decision based on this post as I have no right to advice anyone. This post is just for education purpose only.

SENSEX

75,200

▼ ~1.2% this week

NIFTY 50

23,618

▼ ~1.1% this week

WTI CRUDE

$101+

▲ +60% YoY

USD/INR

~94.96

Rupee under pressure

FPI OUTFLOWS (2026)

₹2.19L Cr

Unprecedented selling

NIFTY P/E

~21x

Still above historical avg

First — Take a Breath

Every few months, Indian markets go through a spell that makes first-time investors feel like the world is ending and experienced investors start second-guessing everything they know. May 2026 is one of those spells.

The Sensex has slipped to around 75,200 and the Nifty is hovering near 23,618. News headlines are alarming. Brokerage alerts are piling up. And everyone from your neighbour to your office WhatsApp group has a theory about why everything is collapsing.

Here’s the truth: the market is not collapsing. It is reacting — rationally and measurably — to a specific set of global and domestic pressures that are identifiable, explainable, and historically familiar. Let’s go through each one, calmly and clearly.

The 5 Real Reasons Markets Are Falling Right Now

🛢️ Crude oil above $100 — India’s biggest vulnerability

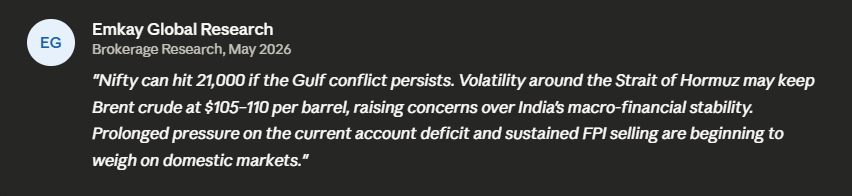

WTI crude crossed $101 per barrel on May 12, with a 10-day high of $113.63. India imports over 85% of its crude oil needs, so every $10 rise in oil prices widens the current account deficit by $14–15 billion. At $100+ oil, analysts project inflation could reach 6.9% — well above the RBI’s 6% tolerance level. The Strait of Hormuz near-shutdown and fragile US-Iran ceasefire are keeping oil elevated with no clear resolution in sight.

💸 FPIs pulling out money at a record pace

Foreign Portfolio Investors have sold a staggering ₹2.19 lakh crore worth of Indian equities in 2026 so far — an unprecedented level of outflows. In May alone, FPI outflows stood at ₹27,048 crore. The combination of crude above $100, rupee weakness, renewed inflation concerns, and valuations that look expensive at ~21x P/E versus North Asian peers is making global funds reduce India exposure. Every rupee of FPI selling puts downward pressure on stock prices and the rupee simultaneously.

🌏 Middle East geopolitics — the Strait of Hormuz factor

The near-shutdown of the Strait of Hormuz — through which roughly 20% of the world’s oil passes — has severely disrupted global energy supply chains. Saudi Aramco’s CEO has warned the market is losing roughly 100 million barrels of oil supply each week. President Trump’s rejection of Iran’s peace proposal and his threat of renewed military action is keeping global risk sentiment deeply negative, triggering sell-offs across Asian equity markets — of which India is a part.

📉 Rising US bond yields & a stronger dollar

Higher US bond yields make US treasuries more attractive relative to emerging market equities — pulling global capital away from countries like India. A stronger dollar amplifies this by making dollar-denominated returns from Indian stocks look less attractive when converted back. This is a classic EM headwind that has triggered outflows from India in 2022, 2018, and 2013 — and it’s repeating now.

📊 Valuation reset — markets adjusting to new reality

Before the oil shock hit, Indian markets were trading at a premium relative to global peers. At ~21x forward P/E on the Nifty, India was priced for near-perfect execution. When a macro shock like $100+ crude arrives, earnings forecasts get cut, and the premium valuation can no longer be justified — leading to a correction. This is not a crash; it’s the market resetting expectations to sustainable levels, as Emkay Global and Kotak have both noted.

What the Experts are actually saying

But here’s what’s holding the market up

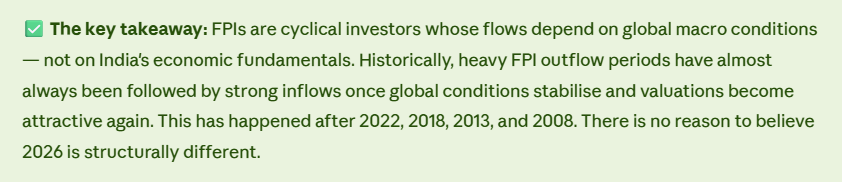

Here’s the part most news articles skip: despite ₹2.19 lakh crore of FPI selling in 2026, the BSE market capitalisation has remained broadly resilient. The Sensex and Nifty are down only around 3% since the US-Iran conflict escalated in February — not the 15–20% crash that the headline numbers might suggest. Why?

Domestic institutional investors (DIIs) and retail SIP investors have absorbed virtually all of the FPI selling. Mutual fund SIPs crossed ₹26,000 crore per month in early 2026 — consistent, systematic buying that has acted as a shock absorber every time FPIs hit the sell button. This is a structural change in the Indian market that didn’t exist a decade ago.

FPI SELLING (2026)

₹2.19L Cr

Record outflows

MONTHLY SIP INFLOWS

₹26,000+ Cr

Record highs

SENSEX FALL SINCE FEB 27

~3%

Despite war escalation

BSE M-CAP RECOVERY

+₹4.18L Cr

Back to pre-war levels

History says: Corrections like this have always Recovered

Let’s look at what happened the last few times Indian markets fell sharply for macro reasons very similar to today’s:

| Period | Trigger | Type | Nifty Peak Fall | Recovery Time |

|---|---|---|---|---|

| 2013 Taper Tantrum | US Fed tightening; FPI outflows; rupee crash to ₹68 | External | −14% | ~6 months |

| 2018 IL&FS + Crude Spike | Oil $80+; NBFC crisis; FPI selling; INR at ₹74 | Mixed | −15% | ~8 months |

| 2022 Ukraine War + Fed Hikes | Crude $130; US rate hikes; FPI exit; rupee at ₹83 | External | −17% | ~10 months |

| Mar 2020 COVID Crash | Global pandemic; markets closed; economy shutdown | External | −38% | ~12 months |

| May 2026 (Current) | Crude $100+; Hormuz closure; FPI outflows; rupee pressure | External | ~−3% so far | TBD — but fundamentals intact |

In every previous instance, investors who stayed invested or added during the dip made significantly better returns than those who sold in panic and waited on the sidelines for the “all clear” signal — which never comes with a loud announcement.

The Sectors Most and Least affected Right now

Not all of your portfolio is equally exposed. Here’s a quick reference on which parts of your portfolio to monitor closely and which to leave alone:

Relatively protected right now

IT & pharma exporters (dollar revenue hedges a weak rupee), upstream oil stocks (ONGC, Oil India benefit from high prices), defence PSUs (government capex-driven, insulated from oil), and gold/gold ETFs (classic inflation hedge performing well).

Under pressure right now

Aviation (IndiGo fell 3.2% on crude spike), oil marketing companies (BPCL, HPCL, IOC down ~1%), jewellery stocks (Titan, Kalyan down 3–4.5%), FMCG and paints (input cost pressure), and rate-sensitive sectors like real estate and consumer durables.

The Bottom Line

Indian markets are falling in May 2026 for five clear, documented, external reasons — crude oil above $100, record FPI outflows, Middle East geopolitical tensions, rising US bond yields, and a valuation reset from elevated levels. None of these are surprises. All of them have historical precedents. And in every previous case, India’s markets recovered — rewarding investors who stayed calm and continued investing over those who panicked and sat on the sidelines.

India’s GDP growth remains above 6.5%, domestic consumption is intact, the government’s infrastructure and defence capex pipelines are fully funded, and the SIP habit of Indian retail investors has fundamentally changed how resilient markets are to external shocks. The fundamentals that made India one of the world’s best-performing major markets over the last decade have not changed. The weather outside is rough — but the house is still standing.

Stay invested. Stay systematic. Don’t let the noise make the decision for you.

Disclaimer: This article is for educational and informational purposes only and does not constitute financial advice. All index levels and market data are approximate. Consult a SEBI-registered financial advisor before making investment decisions. Past performance is not indicative of future returns.

Read More: What Crude Oil Above $90 Means for Your Indian Portfolio

Pingback: SIP vs Lump Sum: Which Strategy Wins Over 10, 20 & 30 Years? - The EquityVerse